Weekly Newletter #41

Ads

Welcome to the first edition of the Trend Tracker newsletter. My weekly service delivers comprehensive research and analysis on S&P 500 index futures. Thank you for taking the time to read it.

The purpose of Trend Tracker is to help you better understand market trends and make more informed decisions for trading and investing. I am excited to launch Trend Tracker, as it represents the culmination of more than 30 years of experience in the financial markets.

Why I Focus on S&P 500 Index Futures

After three decades in the markets, I've come to a simple conclusion: if you want to trade trends systematically, you need deep, liquid markets where price action stays "clean." The S&P 500 futures market - with hundreds of billions trading daily - gives us exactly that.

The constant arbitrage activities between cash, futures, and options keep prices efficient and predictable for systematic analysis. This isn't a market where individual participants can manipulate price action. It's pure supply and demand, driven by the largest, most sophisticated institutions in the world.

That's why legends like Paul Tudor Jones and George Soros have built their fortunes on systematic trend-following in liquid markets. I'm simply adapting their proven approaches for the timeframes that work in today's market environment.

OK, let’s get started.

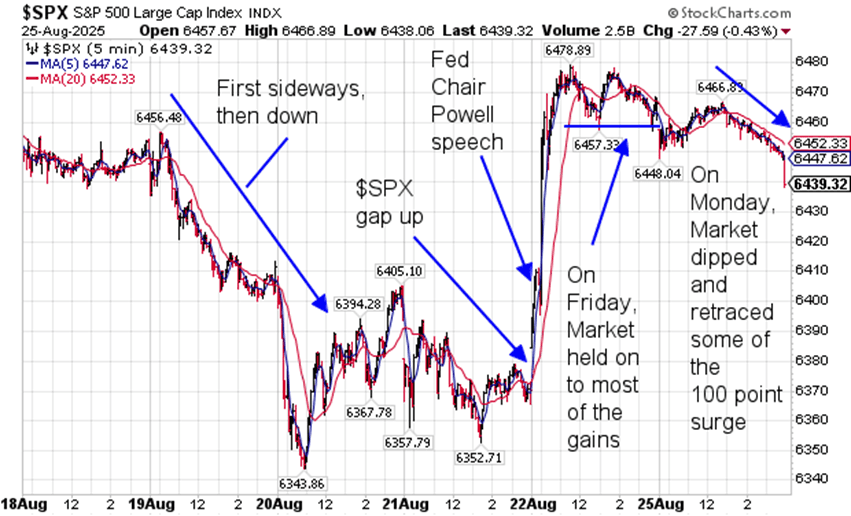

Last week, the market initially moved sideways before turning lower. For two days, the S&P 500 stayed range-bound, trading within a 40-point range. Then, on Friday, it gapped higher and rallied sharply following Fed Chair Powell's speech. On Monday, the market pulled back, retracing some of Friday’s 100-point surge.

Investors had already been expecting the next phase of Fed policy to include interest rate cuts, so the announcement was no surprise. However, hearing it directly from Powell solidified expectations, leaving little room for the Fed to reverse course. The only factor that could derail a rate cut now would be new economic data showing an unexpected spike in inflation.

With stock market valuations already stretched, we plan to take opportunities on both sides of the market - trading long and short positions as conditions warrant.

Last week’s chart for cash market S&P 500 index ($SPX)

chart courtesy of StockCharts.com

Weekly Market Brief: S&P 500 Index Futures (ES / MES)

This past week, the markets were galvanized by renewed expectations of monetary easing as Federal Reserve Chair Jerome Powell delivered cautious yet encouraging remarks at the Jackson Hole symposium. His tone signaled a growing possibility of interest rate cuts, triggering a rebound across equity markets - particularly in S&P 500 futures.

Market Swing and Key Developments

• S&P 500 Futures Movements

Across the week, E‑mini S&P 500 futures realized a modest net gain, continuing recovery from recent soft patches. The benchmark absorbed surging energy in equity markets as investor sentiment improved.

• Fed Signals Lift Market Sentiment

On August 22, Powell acknowledged that 'the balance of risks appears to be shifting' from inflation concerns toward a potentially weakening labor market, a pivot that markets interpreted as a prelude to potential rate cuts. Markets responded vigorously: The Dow popped more than 850 points to record territory, while the S&P 500 and Nasdaq both rallied over 1% as traders recalibrated rate‑cut odds toward the September meeting.

• Key Themes in Powell’s Speech

Powell stressed that policy remains restrictive but evolving conditions 'may warrant adjusting our policy stance,' signaling openness to easing if upcoming inflation and employment data justify it. Markets interpreted this as dovish, pricing in nearly a 90% chance of a September cut.

Fed Can’t Go Back Now

Powell’s remarks underscore a critical shift: the Fed appears disinclined to revert to its previous hawkish stance. By hinting at rate cuts, Powell effectively committed the central bank to navigate forward with easing in mind, making reversal both politically and practically challenging. This 'Fed can’t go back now' dynamic has reshaped expectations, anchoring markets to the belief that the era of rate hikes is likely over - at least temporarily.

Buy the Bad News, Sell the Good?

This week’s price action illustrates a classic contrarian dynamic: 'buy the bad news' - such as signs of weakening labor market - which tends to imply supportive policy from the Fed, boosting equities; 'sell the good news' - better‑than‑expected data - that raises fears of rate persistence, weakening sentiment. Powell’s dovish hints rewarded markets when weaker data seemed more probable, reinforcing this reflexive sentiment play.

Outlook: What to Watch Next

• Incoming Data & Fed Reaction

Markets are now highly sensitive to August’s inflation and jobs data. A cooler CPI/PCE or soft payrolls would likely reinforce rate‑cut expectations and extend the rebound. Conversely, unexpectedly strong readings could dampen enthusiasm.

• Earnings & Tech Sector Focus

With Nvidia and other tech heavyweights set to report, earnings will help determine if this rally legs or relies too heavily on macro optimism.

• Volatility Ahead

Some strategists caution this could be a 'late‑summer rally' - a short‑lived burst of optimism before volatility returns in autumn.

In summary, a dovish Powell set the tone for a decisive turn in sentiment, driving a sharp rally in S&P 500 futures. The narrative now hinges on whether incoming data validates his shift - or threatens to pull the rug out from the rally.

Monday should mark the beginning of a new short-term uptrend. However, this trend is still in its early stages and remains fragile. For it to be validated, the market must continue moving higher. If it fails to do so, opportunities for short selling will likely emerge rather quickly.

by Peter B. Levant, MBA, MSc Finance, Managing Director, Index Research LLC

Weekly Reports

/

Smart market insights

Want us to cover a specific topic?

Whether it’s a sector, company, or macro theme you'd like to see explored — tell us. We continuously refine our research based on member input.