Weekly Newletter #43

Ads

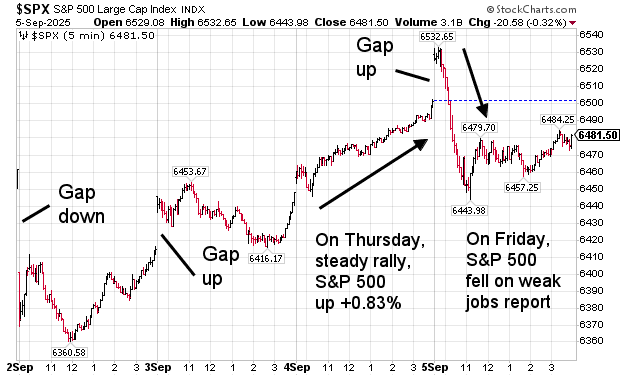

S&P 500 rally intact, but at risk

The S&P 500 initially surged into record territory last week, buoyed by heavy gains in technology and AI-linked names. However, the rally reversed sharply on Friday, after the release of an unexpectedly weak August jobs report. Modest gains over the week were overshadowed by Friday’s pullback as investor sentiment swung. This was a similar pattern to last week.

chart courtesy of stockcharts.com

S&P 500 Performance (September 1-5, 2025)

Day | Date | Closing Level | Daily Move Change |

|---|---|---|---|

Monday | Sep 1 | Market Closed | none |

Tuesday | Sep 2 | 6,415.54 | ↓ -0.69% |

Wednesday | Sep 3 | 6,448.26 | ↑ +0.51% |

Thursday | Sep 4 | 6,502.08 | ↑ +0.83% |

Friday | Sep 5 | 6,481.50 | ↓ -0.32% |

This is as Data Driven as it gets!

The Feds dual mandate will be put to the test as new incoming data will be key factors in determining interest rate policy.

Just as a reminder, this is the Fed’s dual mandate.

Maximum employment (jobs)

The Fed seeks to promote conditions that foster a strong labor market, meaning as many people as possible who want a job can find one. This doesn’t mean zero unemployment, since some level of turnover and job searching is natural, but it means keeping the labor market healthy and resilient.

Stable prices (inflation)

The Fed aims to keep inflation low and stable, which in practice has been defined as a 2% average inflation target over time. This is intended to preserve the purchasing power of the U.S. dollar and provide households and businesses with more predictable economic conditions.

Balancing these two goals is often challenging, but especially now. These two mandates could be in conflict. Recent data suggest that the job market is softening. While inflation has come down, it has been sticky and there is still upside risk.

Jobs / Inflation | Fed policy response |

|---|---|

Job market weakens | Cut |

Inflation rises | Maintain |

Inflation will be key

The biggest threat to the Federal Reserve’s expected easing cycle is inflation. While markets are pricing in a rate cut at the upcoming FOMC meeting, any upside surprise in incoming inflation data could derail or slow the pace of cuts. If consumer price or producer price indices show renewed price pressures, the Fed will be forced to reconsider its stance, prioritizing inflation control over labor market softness. For investors, this makes next week’s CPI and PPI readings critical swing factors - not only for policy direction but also for the sustainability of the recent rally in risk assets.

Market highlights

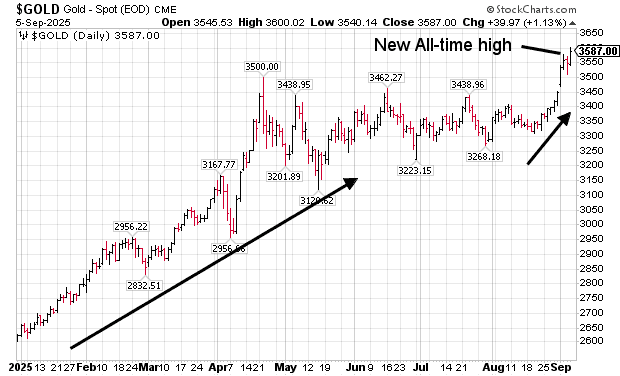

Gold

Gold soared to new all-time highs, reflecting investor demand for safe havens amid growing macroeconomic uncertainty and renewed bets on Fed easing.

chart courtesy of stockcharts.com

U.S. Labor Market

The August nonfarm payrolls figure came in at just 22,000, far below expectations, and revisions to July data were downward. The unemployment rate ticked up to 4.3%. These readings confirmed a significant slowdown in hiring.

Treasury Yields

Yields tumbled in response. The 2-year Treasury yield dropped toward 3.5%, and the 10-year yield fell to around 4.08%, multi-month lows.

Fed Rate-Cut Odds

Expectations for a 25 bp rate cut at the Fed’s September 16-17 meeting are now virtually baked in. According to the CME FedWatch, markets assign nearly 100% odds to that outcome and even some probability at 14% of a 50 bp cut.

AI-Sector Dynamics

AI-related equities helped fuel the rally early in the week - especially after high-profile earnings beats in the tech and semiconductor space. But with valuations stretched, traders appear to be taking profits, signaling a potential cooling-off period for the “AI trade” heading into next week.

Federal Reserve Decision

The Federal Reserve holds its September 16 - 17 FOMC meeting. A 25 basis-point cut is all but certain. Markets are also starting to price in the possibility of a 50 bp cut. Fed Governor Christopher Waller is advocating for multiple cuts starting now, citing the weakening labor market. Other officials, however - including Presidents Musalem and Bostic - are urging caution and additional data before committing to further easing.

U.S. Economic Calendar (September 8–12)

◾Monday: Consumer Credit

◾Tuesday: Redbook

◾Wednesday: PPI & Core PPI

◾Thursday: CPI & Core CPI for August; Weekly Jobless Claims

◾Friday: Michigan Consumer Sentiment

Global & Geopolitical Risks

Markets remain sensitive to Fed independence concerns, political pressure on monetary policy, and geopolitical flashpoints including Europe, U.S.–China dynamics, and ECB policy decisions.

AI Sector and Market Sentiment

AI-fueled enthusiasm has driven tech valuations to lofty heights. With earnings largely priced in, market players may take profits next week, creating near-term consolidation or sector rotation - without abandoning the long-term AI growth narrative.

What to Watch

Last week’s weak jobs data triggered a strong pivot toward Fed easing. Stocks briefly soared before Friday’s sell-off, as markets punished growth concerns. Gold’s break to new highs signals risk-aversion and rising concerns over the durability of the recovery.

Next week looms crucial. A 25 bp cut by the Fed appears locked in, but the bigger question is the trajectory beyond September. The inflation data - particularly CPI - will be decisive. If inflation moderates, the Fed will have the green light to pursue a multi-cut strategy. But if CPI surprises to the upside, the Fed may be forced to temper its easing bias, leaving markets vulnerable to disappointment.

Investors will also parse earnings reports for confirmation of forward earnings growth. The AI sector may pause as markets recalibrate valuations, policy tone, and macro conditions. Meanwhile, defensive positioning - into gold, Treasuries, and utilities - may continue as a hedge against policy missteps or inflation shocks.

In short, while the Fed is on the verge of cutting rates, inflation remains the critical swing factor that could redefine the trajectory of monetary policy and market performance in the weeks ahead.

Trading Perspective

The past two Friday’s, the S&P 500 sold off, indicating that investors are risk-averse to holding long positions over the weekend.

My model’s High Time Frame (HTF) using daily data has the current BUY trend (uptrend) as only two days old and weak. In fact, this reading is almost neutral. From a short-term trend-following perspective, there is almost no trend. Therefore, I am looking to trade on both sides of the market, both BUY (long) and SELL (short).

On the Low Time Frame (LTF), BUY on 2-minut and 5-minute bars, with 5/20 and 10/40 SMA upward crosses. And SELL on 2-minute and 5-minute bars with 5/20 SMA downward crosses.

Remember the importance of time-of-day effects. In general, I concentrate on the market open and the first hour for high-liquidity trading.

by Peter B. Levant, MBA, MSc Finance, Managing Director, Index Research LLC

Weekly Reports

/

Smart market insights

Want us to cover a specific topic?

Whether it’s a sector, company, or macro theme you'd like to see explored — tell us. We continuously refine our research based on member input.