Weekly Newletter #46

Ads

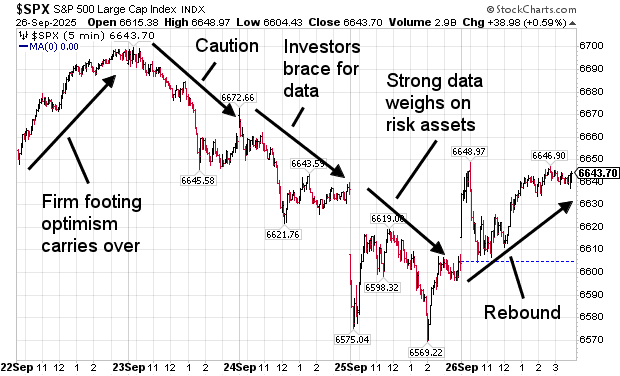

Stocks Rebound After Data-Driven Selloff: S&P 500 Ends Week on a Positive Note

The U.S. stock market experienced a volatile but ultimately stabilizing week, as the S&P 500 navigated a complex mix of economic data releases, Federal Reserve commentary, and shifting investor sentiment. The week featured three consecutive down days from Tuesday through Thursday, raising concerns about whether a short-term correction was forming. Yet Friday’s rebound suggested that, at least for now, equity markets remain resilient in the face of cross-currents.

chart courtesy of stockcharts.com

The central themes were stronger-than-expected U.S. economic data, Federal Reserve Chair Jerome Powell’s cautious remarks about equity valuations, and the market’s ongoing recalibration of interest rate expectations. While robust GDP and consumption data confirmed the U.S. economy remains in good shape, paradoxically this limited the urgency for the Fed to continue cutting rates. Investors were left balancing optimism about economic momentum with the reality of a less dovish monetary backdrop.

Day-by-Day Breakdown

▪ Monday → Market Opens on Firm Footing, Optimism Carries Over

The week began on a positive note, with the S&P 500 rising modestly. Investor sentiment was buoyed by carry-over momentum from the prior week and continued belief that rate cuts, even if gradual, were still on the horizon. Large-cap technology names provided initial leadership, and breadth was supportive across sectors.

▪ Tuesday → Powell’s Valuation Warning Sparks Caution and Profit-Taking

Selling pressure emerged as traders reassessed valuations in light of Powell’s recent comments that stock market levels may be “too high.” These remarks injected a tone of caution and sparked profit-taking, particularly in growth stocks. The S&P 500 closed lower, with defensive sectors showing relative strength while cyclical sectors lagged.

▪ Wednesday → Selling Extends as Investors Brace for Heavy Data Flow

The market extended its decline for a second day, weighed down by cautious positioning ahead of a busy data calendar. Investors rotated into Treasuries, though yields did not collapse, signaling that the bond market still expects moderate growth rather than imminent recession. The S&P 500 index remained under pressure.

▪ Thursday → Strong Economic Data Paradox Weighs on Risk Assets

The week’s most pivotal day brought a flood of U.S. economic data. Durable Goods Orders, GDP, jobless claims, and Personal Consumption Expenditures (PCE) were released. Most indicators surprised to the upside, with GDP in particular showing notable strength. On balance, the data reinforced the view that the U.S. economy remains resilient, with consumer demand intact and labor markets steady. However, the paradox for equities was clear: stronger data meant less urgency for the Fed to cut rates aggressively. Equity markets sold off for a third straight session, as traders digested the implications for risk assets.

▪ Friday → Bargain Hunters Step In, S&P 500 Rebounds into Weekend

Markets finally found footing on Friday. The S&P 500 rebounded as bargain-hunters stepped in after three consecutive down days. The upturn suggested that while valuations are being questioned, selling pressure has not yet turned into broad-based panic. Friday’s rally helped limit the week’s losses and reinforced the sense that the equity market is digesting rather than collapsing.

S&P 500 Weekly Performance

Last week, after the ups and downs, the S&P 500 was down -0.31% and the Nasdaq 100 was down -0.50%.

Economic Data Recap

The economic calendar last week was dense with important releases:

Durable Goods Orders: Showed strength, signaling that business investment remains healthy despite higher financing costs.

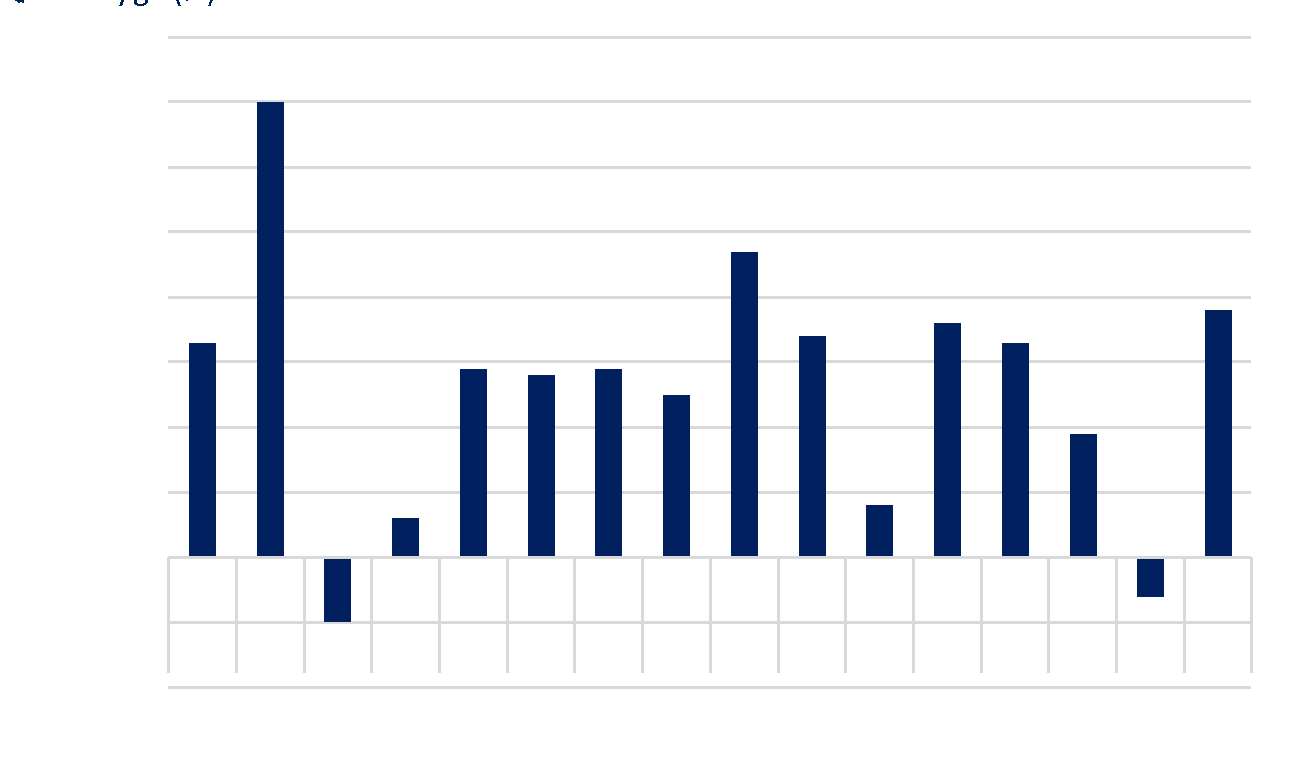

GDP (Q2 revision): Surprised to the upside, underscoring that U.S. growth is holding firm. This was one of the most significant signals for markets, as it reinforced the idea that the U.S. economy is not in bad shape at all.

Jobless Claims: Came in lower than expected, pointing to ongoing labor market resilience.

Personal Consumption Expenditures (PCE): Inflation data remained elevated enough to discourage aggressive Fed easing, though not alarming.

The broad takeaway was that the U.S. economy continues to surprise positively. However, the strength creates a policy dilemma for the Fed. With growth and consumption intact, there is less justification for accelerating the pace of rate cuts. This left investors recalibrating expectations for the trajectory of monetary policy heading into year-end.

The chart below shows Quarterly GDP changes (%).

source Bureau of Economic Analysis U.S. Department of Commerce

Federal Reserve Commentary

Fed Chair Jerome Powell’s comment that the stock market may be “too high” reverberated throughout the week. While the Fed rarely speaks directly about asset valuations, his remark highlighted concerns about speculative excess and overextended multiples, particularly in growth and technology sectors. Combined with the stronger-than-expected data, his tone cooled enthusiasm for equities and reinforced caution about betting on aggressive easing.

For risk assets, the message was mixed: the Fed is not seeking to trigger a downturn, but nor is it inclined to underwrite speculative rallies with rapid cuts. The result was a choppy equity tape, as markets digested the recalibration.

U.S. Treasury Yields

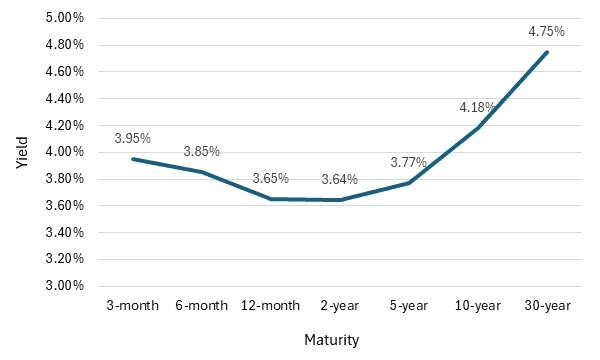

Treasury yields edged higher during the week but did not collapse despite equity volatility. The resilience of yields reflected the stronger economic backdrop. Benchmark 10-year yields remained elevated (4.18%) relative to recent lows, underscoring that bond investors do not anticipate a rapid easing cycle. This is important for equities, as higher yields tend to weigh on valuations by increasing the discount rate for future earnings. However, the fact that yields are not spiking dramatically suggests bond markets are signaling stability rather than distress.

The chart below shows the US Treasury yield curve.

source Bloomberg

Sector and Technology Performance

Technology stocks, which have been the market’s key leadership group for much of 2025, faced headwinds during the week. The combination of Powell’s valuation remarks and stronger data limiting the Fed’s dovishness caused profit-taking in megacap names. While Friday’s rally provided partial relief, the sector still underperformed the broader S&P 500 over the week.

Cyclical sectors such as Industrials and Financials showed relative resilience, benefiting from the stronger growth outlook embedded in the data. Defensive sectors such as Utilities and Consumer Staples attracted some inflows during the midweek sell-off. Overall, sector performance reflected a market which is searching for a balance between growth optimism and valuation discipline.

Investor Sentiment and Market Psychology

Investor psychology last week can be summarized as cautious but not fearful. The three-day decline from Tuesday to Thursday created a sense of vulnerability, especially given Powell’s comments. Yet the rebound on Friday showed that underlying appetite for equities remains intact. The narrative is one of digestion: markets are absorbing a mix of positive economic surprises and the reality of a less supportive monetary policy trajectory.

This Week will be busy again

Looking forward, the economic calendar includes:

Monday | Pending Home Sales |

Tuesday | Redbook |

Wednesday | ADP Nonfarm Employment |

Thursday | Initial Jobless Claims |

Friday | Unemployment Rate |

Markets will remain attuned to Treasury yield movements and any additional Fed commentary, as these continue to be the key drivers of risk sentiment.

Summary

Last week illustrated the push and pull between strong economic fundamentals and cautious monetary policy. The S&P 500 endured three consecutive down days as markets digested Powell’s valuation remarks and a stronger-than-expected data slate. Yet Friday’s rebound showed resilience, suggesting that while investors are re-rating risk, there is no imminent collapse in sentiment.

The U.S. economy remains robust, as evidenced by GDP, consumption, and labor data. The paradox for equities is that such strength diminishes the urgency for the Fed to cut rates, limiting the monetary tailwinds that have historically supported rallies.

Technology stocks, the market’s leadership group, stumbled but did not break. Treasury yields remained elevated but stable, signaling neither crisis nor imminent collapse. The coming week will bring further clarity with fresh data and Fed insight, keeping investors focused on the balance between growth, policy, and valuations.

In short, the equity market is digesting mixed signals but has not lost its footing. Investors should expect continued volatility as the tug-of-war between economic resilience and policy caution plays out.

Trading Perspective

The most notable development this week was Friday’s rebound. From a calendar-effect perspective, the Friday close often carries extra weight.

Based on my high-time-frame (HTF) daily data model, a negative Friday close was needed to confirm a new short-term downtrend. That did not occur, leaving the trend uncertain. The market’s resilience is impressive, particularly given the slow pace of interest rate cuts, ongoing geopolitical risks, and persistent trade tariff headwinds. This is most likely underpinned by generally strong U.S. economic data.

For the coming week, I plan to trade both sides of the market - long and short.

Low-Time-Frame (LTF) signals:

BUY: 2- and 5-minute bars, triggered by upward 5/20 and 10/40 SMA crossovers.

SELL: 2-, 5-, and 15-minute bars, triggered by downward 5/20 and 10/40 SMA crossovers.

I will also consider trading price bounces off either the fast or slow SMA, depending on the speed and context of the crossover.

by Peter B. Levant, MBA, MSc Finance, Managing Director, Index Research LLC

Weekly Reports

/

Smart market insights

Want us to cover a specific topic?

Whether it’s a sector, company, or macro theme you'd like to see explored — tell us. We continuously refine our research based on member input.