Weekly Newletter #44

Ads

S&P 500 Sets Fresh Highs as Rate Cut Bets Intensify

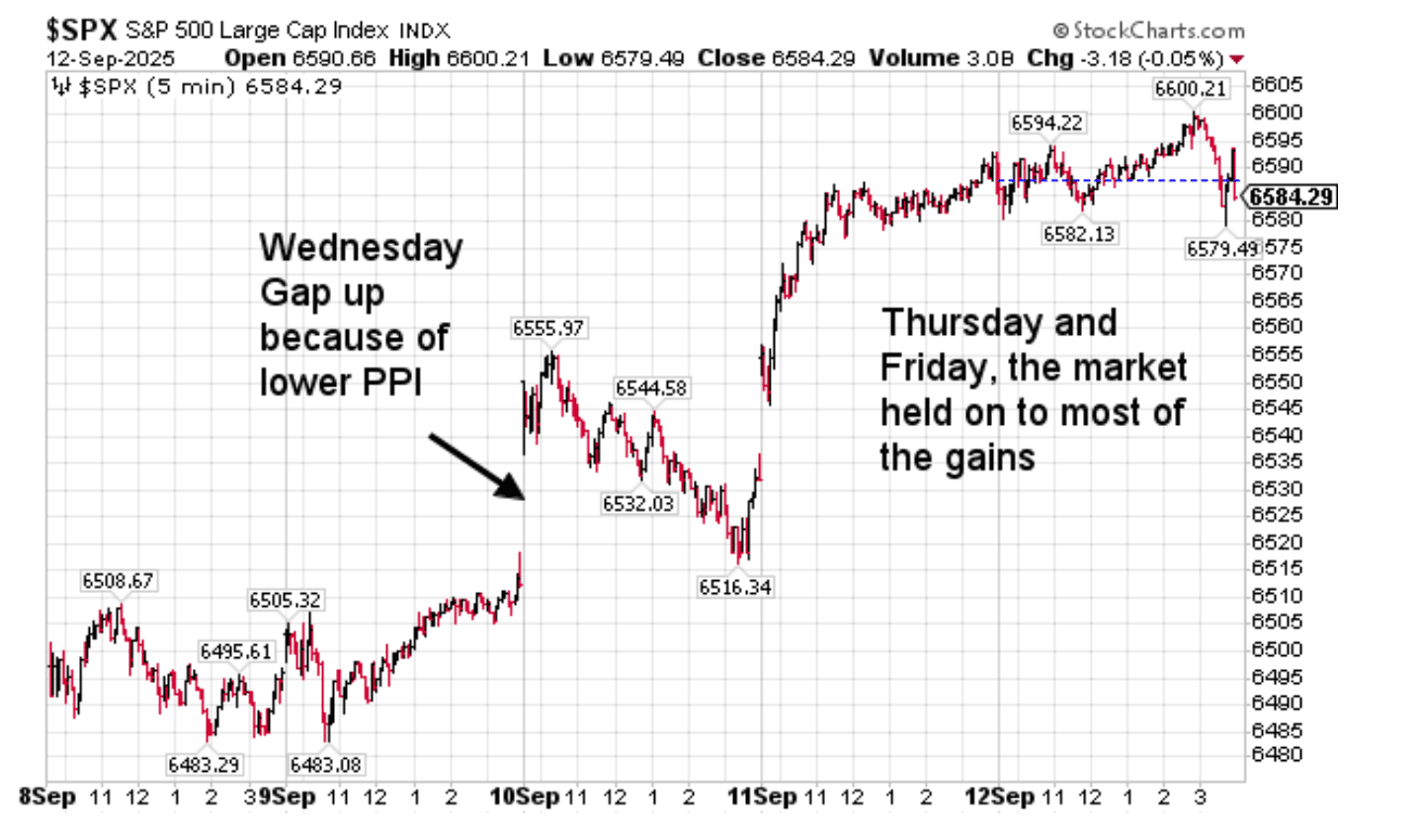

The U.S. equity market capped a strong week with the S&P 500 reaching a new all-time high. The index built on the summer rally that has been fueled by anticipation of monetary easing. Investors are increasingly confident that the Federal Reserve will begin a rate- cutting cycle at its meeting this week, and last week’s economic data only reinforced that expectation.

chart courtesy of stockcharts.com

Inflation Data Supports Fed Easing

Two important reports on inflation - the Consumer Price Index (CPI) and the Producer Price Index (PPI) - came in softer than expected.

• CPI rose 0.4% in August, slightly above the prior month’s +0.2%, but the annual pace is now 2.9%, moving closer to the Fed’s 2% target. Core CPI, which excludes food and energy, rose 0.3% month-over-month and 3.1% year-over-year, signaling modest underlying pressures.

• PPI surprised on the downside, falling 0.1% month-over-month, with core measures also subdued. This easing in wholesale prices suggests input-cost inflation is abating further down the supply chain.

The combination of CPI stability and PPI softness bolstered confidence that inflation is not re-accelerating. Markets responded by pricing in a near-certain 25 basis point rate cut at the September Federal Open Market Committee (FOMC) meeting.

Fed Policy Outlook

The Fed will meet this week to announce its latest policy decision. Futures markets now imply that a cut is fully priced in, and the focus has shifted to the pace and scope of additional easing. Investors are asking: will the Fed signal a one-and-done approach, or will it open the door to a sequence of cuts extending into 2026?

The yield curve is responding accordingly. Treasury bill prices have fallen (short-end yields rose earlier in anticipation of high carry costs), but longer-term yields have eased more gradually, leading to a steepening of the yield curve. The 10-year Treasury yield fell. This steepening reflects an expectation that near-term policy rates will decline while longer-term growth and inflation remain resilient.

Equity Market Leadership

The S&P 500’s new high was once again led by technology and growth names, though leadership is beginning to broaden.

• Mega-cap technology stocks - especially those tied to artificial intelligence - extended gains, with semiconductor and cloud-computing firms leading the charge. Oracle’s strong earnings report added momentum, highlighting resilient demand in enterprise software and AI infrastructure.

• Other sectors also participated: financials benefited from the steepening yield curve, which improves lending margins, while industrial and materials stocks rallied on expectations of stronger demand if monetary policy eases.

• Still, technology remains the dominant driver. The “Magnificent Seven” continue to account for a disproportionate share of S&P 500 gains, though incremental support from cyclicals suggests the rally is becoming somewhat healthier.

The key question for investors is whether this rally can broaden further. If rate cuts succeed in extending the economic cycle, leadership may shift toward cyclical sectors such as financials, industrials, and consumer discretionary. For now, however, Big Tech is still setting the pace.

Cross-Asset Signals

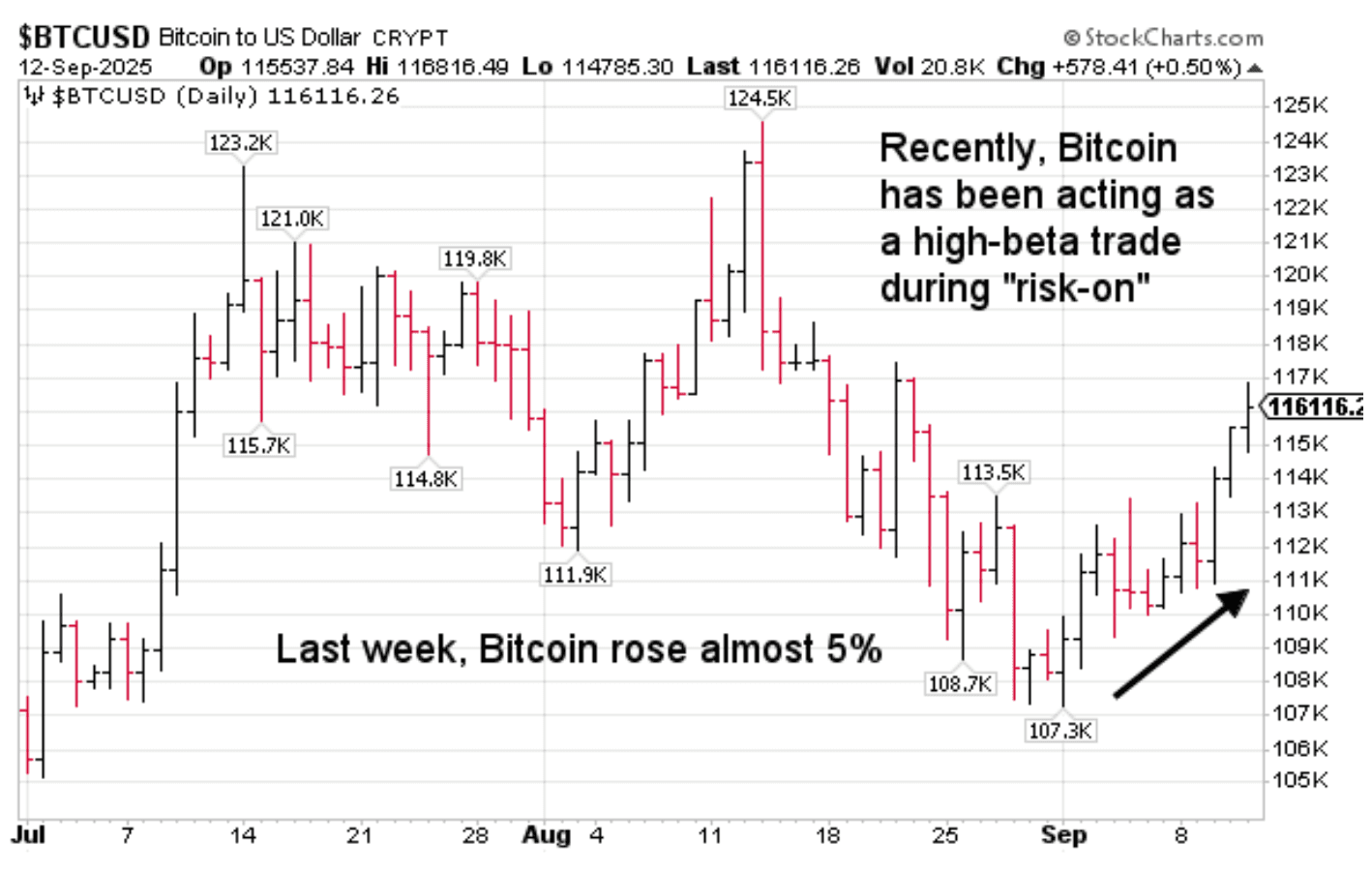

Equities were not the only asset class to rally last week. Gold and Bitcoin surged, both benefiting from expectations of easier U.S. monetary policy and a weaker dollar.

• Gold is hovering near record levels as real yields decline and demand for hedges against policy uncertainty rises.

• Bitcoin’s price rose and most recently it has been acting as a high-beta trade when investors are “risk-on.”

chart courtesy of stockcharts.com

These moves suggest markets are positioning for abundant liquidity and a renewed appetite for alternative assets once rate cuts begin.

What’s on the Calendar This Week

This week brings a critical set of events that could define the market’s trajectory into year-end:

1. Federal Reserve Policy Announcement (Wednesday)

A 25 basis point cut is widely expected.

Market focus will be on the dot plot, Chair Powell’s press conference, and forward guidance on whether additional cuts are likely in 2025.

2. Housing Market Data

Existing home sales and housing starts will provide insight into whether falling mortgage rates are reviving housing activity.

3. Labor Market Releases

Jobless claims and regional Fed surveys will offer timely updates on labor conditions, a critical variable for the Fed’s dual mandate.

4. Corporate Earnings Highlights

While earnings season is mostly complete, several bellwether companies in consumer discretionary and technology will report results, providing additional data points on spending and demand trends.

Risks and Considerations

While the market narrative remains constructive, several risks should not be overlooked:

• Valuation Risk: The S&P 500 currently trades at historically elevated multiples, especially in technology. Any disappointment in earnings or Fed guidance could prompt volatility.

• Inflation Stickiness: Shelter and services inflation remain stubborn. If inflation data re-accelerates in the fall, the Fed may slow its easing pace.

• Global Uncertainty: Trade policy, geopolitical tensions, and energy markets remain potential headwinds.

Bottom Line

Last week’s market action underscored a turning point for monetary policy. The S&P 500 hit a record high as inflation data validated expectations of Fed Easing. Technology stocks continue to dominate leadership, but early signs of rotation suggest a broader base of support may emerge. Other assets - from gold to Bitcoin - are rallying in anticipation of liquidity injections, while the Treasury curve steepens on expectations of imminent rate cuts.

The Fed’s policy decision this week will be the defining event. The rate cut itself is already priced in; the market’s reaction will hinge on Powell’s tone and the outlook for further easing. A dovish Fed could sustain risk appetite through year-end, while a more cautious stance may trigger short-term volatility.

For now, the market’s message is clear: investors are positioned for easing and risk assets are responding accordingly.

Trading Perspective

My model’s High Time Frame (HTF), based on daily data, currently shows a BUY trend (uptrend) that is seven days old and demonstrating solid strength. From a short-term trend-following perspective, this environment typically favors continuation, so I am primarily looking to trade from the long (BUY) side. Absent any major surprises, the market is more likely to continue higher.

This week’s Federal Reserve interest rate decision is a key market event. A 25-basis-point cut is already priced in, but investors are watching for signs of a more dovish policy shift. The risk remains that Powell’s press conference may not meet those expectations, potentially sparking a “sell-the-good-news” reaction. I will be watching out for this as well.

Remember that market makers and other short-term traders often exit positions and cancel resting orders in the electronic order book ahead of major announcements (such as this week’s Fed policy decision). When liquidity thins, it can create “air pockets,” with prices whipping violently and skipping levels. Temporary dislocations make price action disorderly, so use caution - stops may be triggered, and market orders can be filled at unfavorable prices.

On the Low Time Frame (LTF), BUY on the 1- , 2- and 5-minute bars, using upward crossovers in the 5/20 and 10/40 SMAs.

Finally, if significant price gaps occur in $SPX (S&P 500 index cash market) this week, I will be looking for “gap-fill” opportunities and plan to execute trades using moving average crossovers aligned with those types of setups.

by Peter B. Levant, MBA, MSc, Managing Director, Index Research LLC

Weekly Reports

/

Smart market insights

Want us to cover a specific topic?

Whether it’s a sector, company, or macro theme you'd like to see explored — tell us. We continuously refine our research based on member input.